In last month’s article, we examined the investment thesis underpinning industrial base metals, specifically focusing on the structural supply deficits and accelerating demand shock within global copper markets. As global power grids undergo a multi-trillion-dollar modernization and electrification cycle due to the development of artificial intelligence (AI), copper has firmly established itself as the bedrock of physical infrastructure.

This month, we shift our focus further down the periodic table to an asset class that occupies a unique, hybridized position in global capital markets: precious metals. While base metals like copper are valued strictly for their industrial utility, precious metals are increasingly behaving as dual purpose assets. They sit precisely at the intersection of two powerful macro dynamics, acting simultaneously as an irreplaceable monetary hedge and a critical industrial input for next-generation technology.

The global economy is entering a regime characterized by persistent fiscal deficits, sovereign debt expansion, and a structural re-shoring of strategic, advanced manufacturing. In this environment, the traditional lines separating monetary safe havens from cyclical industrial commodities are blurring. By examining the dual nature of gold, silver, platinum, and palladium, we can construct portfolios that are resilient against monetary debasement while remaining strategically exposed to the secular growth of AI and advanced computing.

The Legacy of Sovereignty (The Monetary Hedge)

For millennia, precious metals have served as the ultimate form of pristine collateral and a borderless store of value. Unlike fiat currencies, which are subject to the political and fiscal whims of central banks and sovereign treasuries, physical gold and silver possess an inherent sovereignty. They carry no counterparty risk, they share a scarcity factor and cannot be arbitrarily printed into infinity, and maintain total independence from the centralized banking architecture.

In an era defined by aggressive monetary intervention and unprecedented global debt-to-GDP ratios, these foundational characteristics are more relevant than ever. Investors view the monetary aspect of precious metals not as a speculative trade, but as a critical mechanism for portfolio hedging and long-term capital preservation. This protective posture relies on three core institutional pillars:

- Absolute Scarcity: The planetary crust contains a finite layout of these elements, and the capital expenditure required to locate, extract, and refine them ensures that annual supply growth remains constrained to growth in supply of roughly 1% to 2% globally.

- Tangible Permanence: Physical precious metals are virtually indestructible, dense stores of value that do not degrade over centuries.

- Total Sovereignty: They represent a decentralized asset class that is outside the liability loop of the global financial system, providing an essential buffer when trust in sovereign credit wavers.

While gold and silver are the historical archetypes of this monetary legacy, the modern financialization of the platinum and palladium has followed a similar trajectory. The monetary integration of platinum dates back nearly two centuries; Russia minted the first official platinum coins for circulation in 1828, recognizing its immense density and rarity as a natural extension of sovereign wealth.

Palladium underwent its own financialization process in the 1970s. As Western nations instituted the first strict automotive emission standards, the metal transitioned from an obscure laboratory element into a financialized macro asset. The sudden, exponential rise in demand for palladium in catalytic converters transformed it into a deeply liquid, traded commodity, drawing massive institutional inflows and establishing it as a staple of modern commodity exchanges.

The Tech-Industrialization Engine

While the monetary narrative provides a solid floor for valuation, an emerging alpha engine for precious metals in the coming decade lies in their rapid technologization. The global economy is currently undergoing a massive structural shift driven by AI, cloud computing architectures, high-performance semiconductors, and complex telecommunications hardware. This technological leap forward has permanently altered the demand equation for precious metals.

These elements are no longer just static stores of value locked away in central bank vaults or worn as jewelry. Instead, they have become highly critical, highly specialized industrial inputs. The physical, chemical, and electrical properties of precious metals make them completely irreplaceable in the manufacturing of high-end hardware.

As hyperscale data centers expand to support LLMs (Large Language Models) and advanced neural networks, the demand for components that can handle extreme power densities without failing has skyrocketed. From usage in advanced chip packaging to the intricate circuitry of autonomous vehicle sensors, next-generation technology requires materials that can perform flawlessly under immense thermal and electrical stress. Precious metals are the enablers of this computing revolution, making their market dynamics increasingly sensitive to global technology capex cycles.

Deep Dive: The Big Four Precious Metals

Each metal commands a distinct, irreplaceable operational niche within advanced manufacturing:

- Gold: Prized for its zero-corrosion property and extreme reliability in high-end micro-electronics. It is heavily utilized in bonding wires and electrical contacts within advanced microprocessors, eliminating the risk of signal latency or system failure from chemical degradation over decades of continuous operation.

- Silver: Possesses the highest electrical and heat conductivity of any element on Earth, making it a fundamental requirement for green energy and complex circuitry. Millions of ounces are consumed annually in the production of photovoltaic solar cells, high-spec printed circuit boards, and 5G telecommunications infrastructure.

- Platinum: Crucial for its exceptional thermal and magnetic stability in heavy industrial and high-performance computing applications. It allows critical hardware components, such as high-density hard disk drives (HDDs) and specialized aerospace sensors, to maintain their physical structure and data integrity under extreme heat and stress.

- Palladium: Essential for its unique high-temperature stability within microscopic physical structures and advanced tech components. It serves as an indispensable input for multi-layer ceramic capacitors (MLCCs) and semiconductor plating, ensuring that next-generation computing chips do not warp or fracture during intense processing cycles.

Recent Spot Prices (Kitco 7-22-26)

- Gold: ~$4,100–$4,150/oz

- Silver: ~$59–$60/oz

- Platinum: ~$1,640–$1,670/oz

- Palladium: ~$1,300–$1,350/oz (up ~2–3%)

Key Recent Developments (2025–Mid-2026)

- Historic 2025–Early 2026 Rally: All four metals surged dramatically due to safe-haven demand, central bank buying (especially gold), supply concerns, and broader “debasement trade” amid high debt and geopolitical tensions. Gains included ~65%+ for gold, much higher for silver (~150–170%) and platinum. Palladium also rallied sharply but from lower bases

- Mid-2026 Pullback: Prices declined notably from peaks. Factors included the U.S.-Iran conflict (e.g., Strait of Hormuz disruptions spiking oil/inflation), expectations of higher Fed rates (increasing opportunity costs for non-yielding assets like gold), stronger dollar/yields, and some profit-taking after the rapid run-up. Gold dipped toward $4,000 or below; silver saw sharper drops.

- Recent Rebound (July 2026): Metals have stabilized or risen in July, with silver often outperforming. Drivers include cooling inflation signals, resilient economic data mixed with rate-hike repricing (some scaling back of September interest rate hike expectations), elevated oil, and hopes for Middle East de-escalation/ceasefire talks boosting safe-haven flows. Central bank demand remains a long-term tailwind for gold despite some pauses (e.g., Russia selling some of its holdings).

Bottom Line For Servant Financial Clients

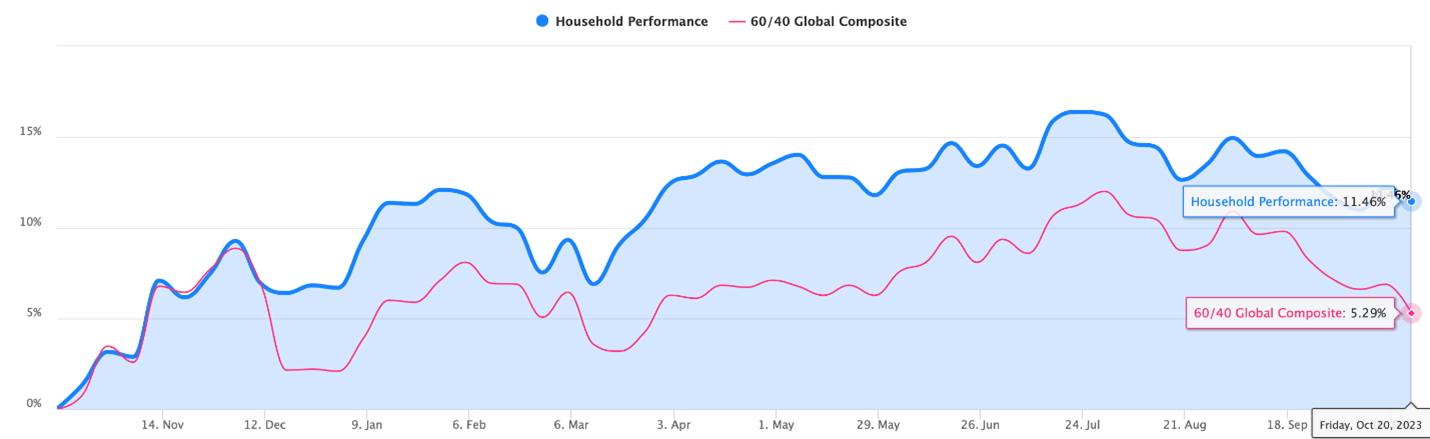

Servant Financial client portfolios have long held, meaningful allocations to gold and other precious metals which has generally led to client risk-based models outperforming traditional 60/40 (equity/fixed income) portfolios. In our October 2023 article Got Gold?, we highlighted that most American household (close to 90%) do not own gold.

Servant Financial clients can assuredly answer affirmatively to having gold ownership. We continually rebalanced client portfolios over the holding period. Further, we roughly halved gold allocations during the runup period in precious metals.

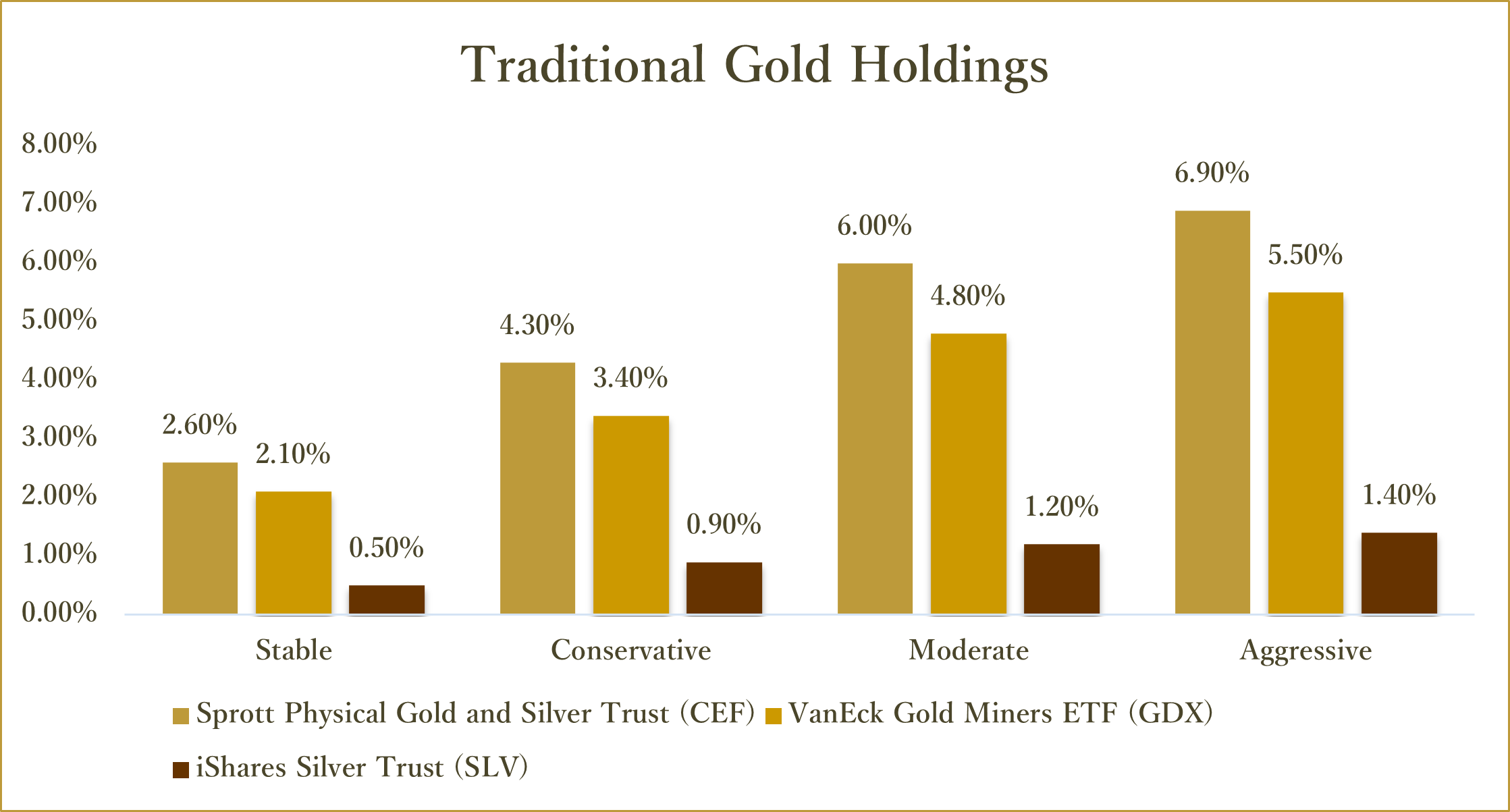

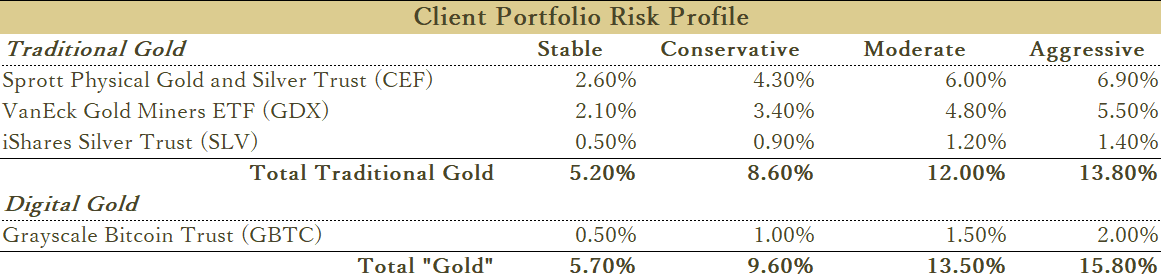

Below is an updated summary of gold allocations by client portfolio risk profile:

Traditional Gold |

Symbol |

Stable |

Conservative |

Moderate |

Aggressive |

|||||

| Sprott Physical Gold & Silver Trust | CEF | 1.40% | 2.20% | 3.00% | 3.4% | |||||

| VanEck Gold Miners ETF | GDX | 1.10% | 1.80% | 2.40% | 2.80% | |||||

| iShares Silver Trust | SLV | 0.60% | 0.90% | 1.20% | 1.40% | |||||

| Total Traditional Gold | 3.10% | 4.90% | 6.60% | 7.60% | ||||||

| Fidelity Bitcoin Fund | FBTC | 1.00% | 2.00% | 3.00% | 4.00% | |||||

| Total Gold | 4.10% | 6.90% | 9.60% | 11.60% |

The allure of gold, gold miners, and other scarce stores of monetary value remains while the growth in demand for precious metal’s technological/industrial applications is an enticing extra benefit. Gold, precious metals and digital gold equivalents, like bitcoin, offer investors a timeless refuge, especially in an era characterized by economic uncertainties, inflation, geopolitical unrest, and rapid innovation.

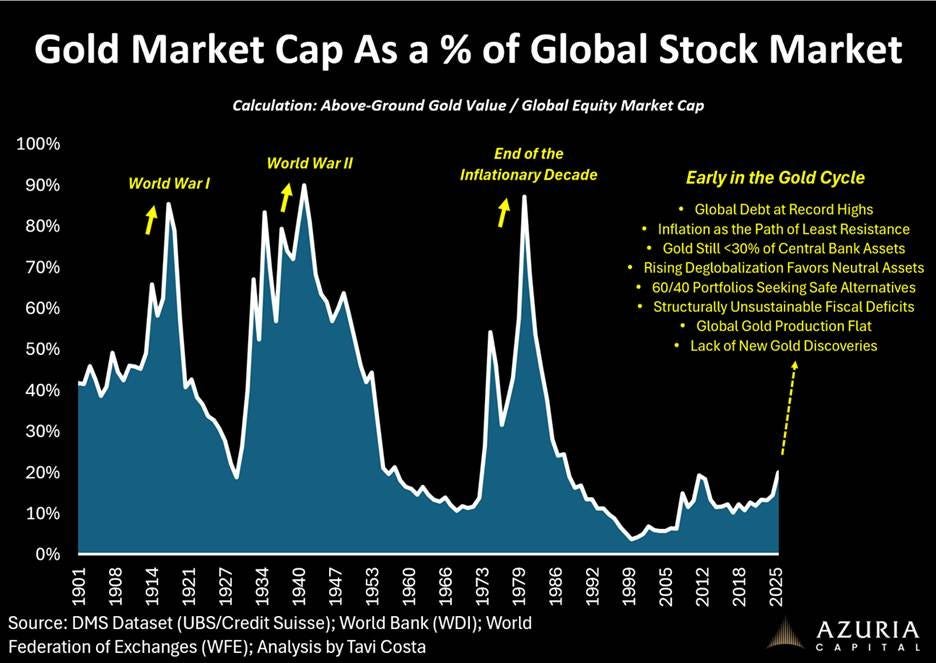

As the following chart suggests, if history rhymes rather than repeats, then we may be early in the current gold cycle.

Source: Tavi Costa via Substack

Clear signs of an impending Fed policy mistake would lead us to aggressively consider a tactical allocation to commodities through PDBC. One low-probability scenario would be a significant dislocation or lack of market liquidity in the U.S. Treasury market that forces the Fed to purchase treasuries. The Fed would effectively be adopting yield curve controls, much like the recent

Clear signs of an impending Fed policy mistake would lead us to aggressively consider a tactical allocation to commodities through PDBC. One low-probability scenario would be a significant dislocation or lack of market liquidity in the U.S. Treasury market that forces the Fed to purchase treasuries. The Fed would effectively be adopting yield curve controls, much like the recent