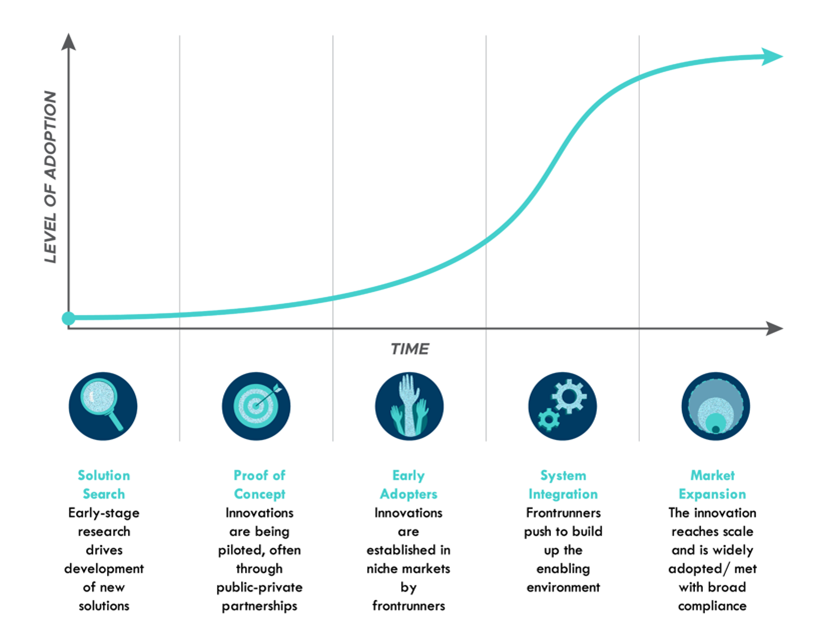

Over the past twelve months, our research has remained focused on a central theme: identifying structural bottlenecks across the global economy and investing in the technological and physical innovations poised to break through or bypass them. We are witnessing a rapidly accelerating paradigm shift. Legacy systems — in energy distribution, financial settlement, and industrial supply chains — are increasingly hitting physical and operational limits. In this environment, a clear understanding of the macro trends reshaping our world is essential. Positioning investment portfolios well for the evolution of these trends requires bridging the physical constraints of the material world with the programmable efficiency of the digital age.

We believe this trend convergence rests on five core pillars:

- Physical Foundations: Critical minerals, chemical reagents, and agricultural inputs

- Monetary Anchors & AI Hardware: Precious metals powering artificial intelligence

- Digital Base Layers: Bitcoin as a digitally native savings device

- Frictionless Settlement: Stablecoins exporting dollar dominance

- Capital Efficiency: Tokenization Real-World Assets (RWAs)

Physical Foundations

The transition to next-generation technologies — renewable energy infrastructure (particularly solar as we’ve highlighted in previous articles), data centers, and AI compute — demands an unprecedented volume of physical, raw materials and input. Over the past year, we have repeatedly highlighted growing supply-demand imbalances in critical minerals such as copper, nickel, cobalt, and lithium. Equally important are the second-order effects. The global reagent squeeze, particularly sulfuric acid — a non-substitutable chemical required to process nearly all critical minerals — illustrates how concentrated and vulnerable certain supply chains remain. By identifying these chokepoints, investors can position capital in specialized manufacturers and infrastructure providers that serve as the essential “picks and shovels” for the broader critical minerals and automation boom. This approach reduces direct commodity volatility while capturing the structural opportunity.

Another stark example of physical vulnerability is the global agricultural supply chain. The 2026 conflict in Iran and the effective closure of the Strait of Hormuz triggered a major disruption in the fertilizer market. The Gulf Region accounts for 46% of global urea trade and at least 20% of seaborne fertilizer exports. Fertilizer production is also heavily dependent on liquefied natural gas. With shipping routes blocked during critical planting seasons, natural gas, fuel, and granular urea prices spiked dramatically. Farmers who had not secured inputs in advance faced sharply higher costs or reduced yields. This episode underscores a key truth: global food security is inextricably linked to secure energy markets and reliable transit corridors. From an investment perspective, it reinforces the need to support domestic, vertically integrated agricultural producers and food supply chains that are insulated from distant geopolitical risks. We expect national champions in food security to emerge in the years ahead.

Monetary Anchors & AI Hardware

Even as the economy digitizes, the role of physical stores of value has intensified. Persistent inflation, rising sovereign debt, and geopolitical instability — including the recent disruptions in the Middle East — continue to drive demand for gold and silver. A powerful new tailwind is emerging: precious metals are transitioning from pure monetary hedges into critical components of the AI hardware stack.

- Silver possesses the highest electrical and thermal conductivity of any metal, making it indispensable for thermal interface materials, cooling systems, and high-conductivity interconnections in data centers and advanced GPUs.

- Gold offers unmatched corrosion resistance and conductivity, essential for high-reliability wiring and plating in memory chips and AI servers.

As AI infrastructure scales, baseline industrial demand for both metals is rising structurally. Investors now gain a dual benefit from precious metals exposure: protection against monetary risk and direct participation in the buildout of both digital AI (cloud-based Large Language Models (LLMs)) and physical AI (robotics and autonomous systems).

Digital Base Layers

If gold is the analog anchor for savings, Bitcoin has established itself as the leading digital savings device and store of value. The era of skepticism that kept many traditional investors on the sidelines is ending. Professional wealth managers who once restricted access — notably Vanguard and Merrill Lynch — have reversed course. In December 2025, Vanguard began allowing trading of third-party bitcoin and crypto ETFs on its platform. In January 2026, Bank of America/Merrill Lynch expanded access, enabling its financial advisors to proactively recommend specific spot Bitcoin ETFs with suggested portfolio allocations between 1% to 4% as suitable for clients.

Bitcoin has matured into a recognized institutional asset class. Operating on a decentralized, immutable, globally accessible ledger, it offers mathematically enforced scarcity and protection from discretionary monetary policy. With accelerating institutional adoption and anticipated regulatory clarity (including potential passage of the CLARITY Act this summer), Bitcoin is solidifying its position as a foundational layer of the future financial stack and a pristine collateral asset for the digital age.

Frictionless Settlement

While Bitcoin serves as the digital store of value, stablecoins are transforming the day-to-day transaction and settlement layer of global finance. Traditional cross-border payments rely on slow correspondent banking, paper records, and high costs. Dollar-pegged stablecoins solve these frictions by bringing fiat currency onto blockchain rails, enabling near-instantaneous, borderless settlement. Supported by landmark legislation such as the GENIUS Act and the anticipated CLARITY Act, stablecoins are not competing with the U.S. dollar — they are extending the dollar’s dominance into the digital realm. Anyone with an internet connection can now access dollar-denominated value and transact globally, 24/7, bypassing limiting factors imposed by legacy systems.

Capital Efficiency

The tokenization of real-world assets (RWAs) is the logical extension of moving money on-chain by also bringing the assets that are purchased with money on-chain. Tokenization of equities, bonds, private credit, real estate, and other traditional assets promises to unlock the next wave of capital efficiency. Legacy markets suffer from multi-day settlement lags, fragmented liquidity, and high administrative overheads.

Tokenization delivers:

- Instantaneous settlement and reduced counterparty risk

- Automated compliance and distributions via smart contracts

- Greater transparency and direct ownership

- Access to previously illiquid assets for a global investor base

As platforms secure necessary regulatory approvals as transfer agents and broker-dealers, the tokenization of RWAs will merge the reliability of traditional assets with the speed and programmability of blockchain technology.

Bottom Line for Servant Financial Clients

Understanding these macro trends is only the beginning. Translating them into actionable portfolio themes for clients is what really matters in the long run. We continue to position client portfolios with targeted exposure across the foregoing five pillars:

- Digital Savings & Settlement: Client spot Bitcoin ETF allocations are obtained through Fidelity Bitcoin Trust ETF (FBTC). Energy first, Bitcoin miner and AI data center developer HUT 8 Corp (HUT), Bitcoin and crypto exchange operator Coinbase Global, Inc. (COIN), and Circle Internet Group (CRCL),the leading U.S. regulated vehicle for stablecoin adoption, enhance client exposure to digital asset settlement and infrastructure layers.

- Physical Foundations & Second-Order Effects: Base precious metals exposures anchor client portfolios through allocations to Sprott Gold and Silver Trust (CEF), Van Eck Gold Miners ETF (GDX), and iShares Silver Trust (SLV). High-quality mining and refining operations for critical minerals through our Forge Ahead sleeve capitalizes on the reindustrialization and onshoring of strategic minerals production. Finally, client exposure to next generation AI autonomy is obtained through Baron First Principles ETF (RONB), complimenting the Forge Ahead thesis through pre-merger access to both SpaceX and xAI private securities and Tesla, Inc. (TSLA).

More recently, we took toehold positions only within our most risk tolerant client portfolios to Black Diamond Group Limited (BDIMF) as a play on near site or on-site housing solutions for large, skilled labor forces needed for data center, industrial production, refining, and manufacturing facilities construction, and the enabling energy infrastructure to power these facilities, and to Ecovyst, Inc. (NYSE: ECVT), a focused play on sulfuric acid and mining reagents.

- Capital Efficiency: Securitize, Inc. through its pending Special Purpose Acquisition Company (SPAC) listing as Cantor Equity Partners II, Inc. (CEPT) has been identified as the premier, U.S. listed platform for the emerging tokenization of RWAs. We have not yet instituted a CEPT position in any client portfolios.

Several entrepreneurs have created vast economic value across America’s almost 250-year history by identifying and resolving the limiting factors that prevent the evolution from the current process state to a more optimal system design. By anchoring portfolios at the intersection of physical scarcity and digital innovation, we believe we have positioned client portfolios well to navigate and capitalize on the inherent productivity gains that can be achieved from eliminating systemic bottlenecks and strategic dependencies.